Space-Enabled Device-to-Device Convergence: An Under-Recognized Inflection in Future Connectivity

The fusion of space-based internet infrastructures with terrestrial 6G networks is setting the stage for a profound structural shift in global connectivity paradigms. Beyond incremental enhancements in speed or device proliferation, the emerging capability of Device-to-Device (D2D) communications directly via satellite constellations may disrupt current network architectures, capital allocation models, and regulatory frameworks over the next 10 to 20 years.

This paper identifies the nascent convergence of space-ground D2D communication—propelled by developments in 6G commercialization and mega-constellations like Starlink—as a genuinely underappreciated inflection point. This evolution heralds an architectural leap towards fully integrated, hyper-resilient, and ubiquitous connectivity ecosystems, with implications that extend well beyond the telecom sector into automotive, industrial Internet of Things (IoT), and regulatory governance domains.

Signal Identification

The integration of space-based broadband constellations enabling Device-to-Device (D2D) communication with terrestrial 6G networks qualifies as an emerging inflection indicator. It is neither widely recognized nor mainstream in policy or capital markets despite its high potential impact. This signal is characterized by its cross-sector reach—telecom, automotive, aerospace, IoT, and regulatory environments—and its potential to restructure core network dependencies.

Time horizon for plausible structural shift is 10–20 years, aligning with projected mass 6G deployment and maturing satellite technology convergence around 2030 (ITU Hub 09/04/2026). Plausibility band is rated high given ongoing investments by major global players, including SpaceX’s Starlink and standardization bodies advancing protocols for integrated services in the 6G era (TechFueler 15/03/2026).

Exposed sectors include telecommunications infrastructure, IoT industrial applications, automotive (notably autonomous vehicles and robotaxis), aerospace, and regulatory bodies overseeing spectrum and data governance.

What Is Changing

The traditionally siloed domains of space-based internet and terrestrial mobile networks are converging through D2D communication capabilities that directly link devices via satellite constellations without intermediary ground stations. This signals a shift away from centralized core networks towards flexible, distributed connectivity models (ITU Hub 09/04/2026).

Starlink’s low-latency mega-constellation, originally designed to serve underserved or rural areas, is now positioning to integrate with terrestrial infrastructures and smart connected devices, including Tesla vehicles and robotaxis (Securities.io 14/04/2026). This suggests a future where mobility and connectivity are seamlessly intertwined, enabling persistent, device-level internet connectivity regardless of geographic constraints.

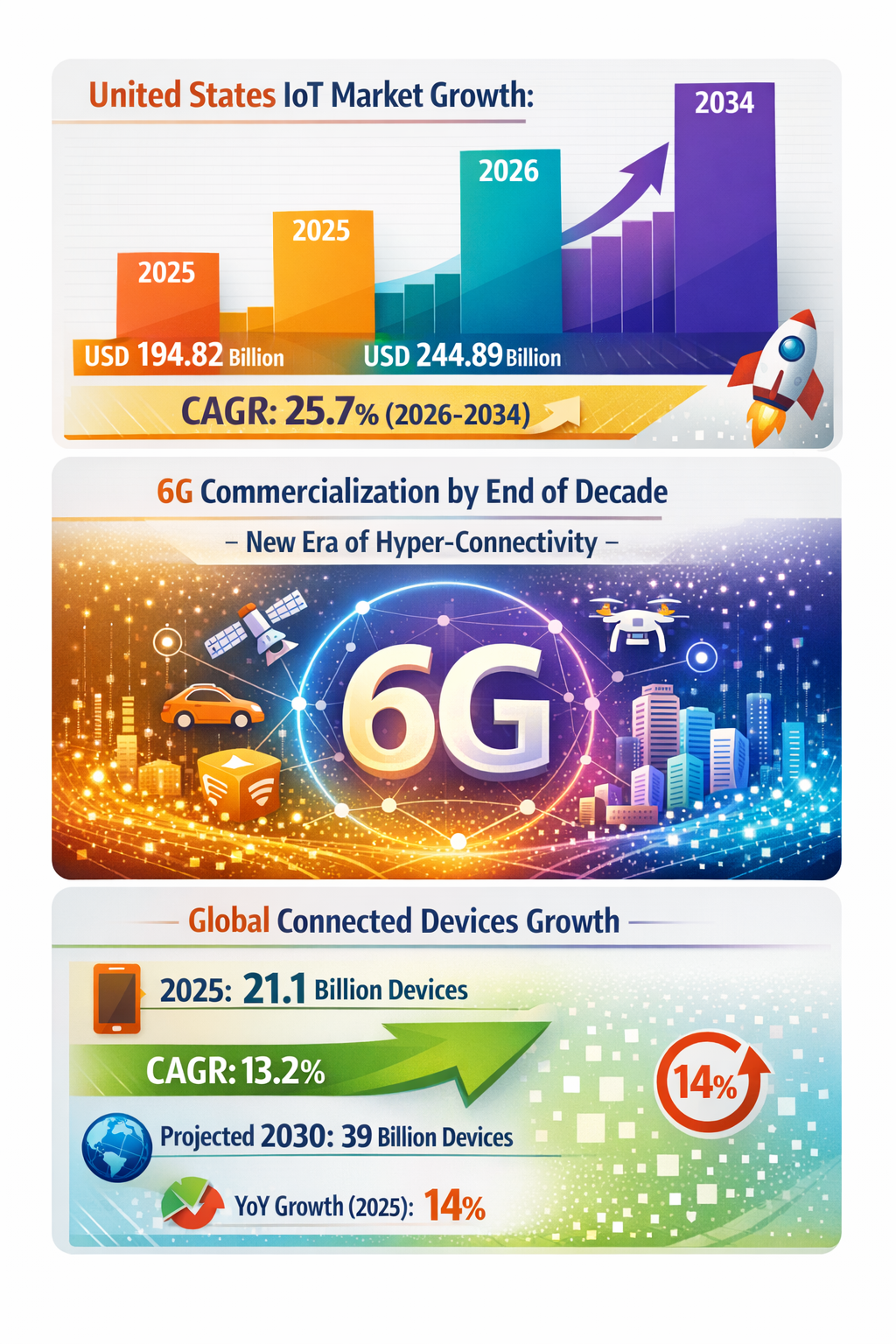

The explosive growth projections for IoT devices—from 21.1 billion connected units at the end of 2025, forecasted to nearly double by 2030, to the U.S. IoT market hitting $1.5 trillion by 2034—highlight increasing demand for robust, ubiquitous connectivity capable of supporting industrial, consumer, and mobile use cases (Stingrai.io 04/2026; Market Data Forecast 10/04/2026).

Simultaneously, next-generation 5G systems are entering a phase prioritizing standalone adoption and ecosystem readiness. Yet they reveal limitations in coverage and resilience, especially for mission-critical IoT and vehicular use cases (GSA Comm 20/04/2026). D2D over satellite integration offers a distinct qualitative leap, enhancing redundancy and lowering latency by sidestepping congested terrestrial backhauls.

Collectively, this indicates a substantive structural theme: the imminent rise of a converged space-terrestrial connectivity fabric enabling direct device communication, transforming network topology, resilience, and value chains.

Disruption Pathway

This signal could evolve structurally through sequential dynamics aligned with technology maturation, standards development, and regulatory adaptation. Initial acceleration would stem from pilot deployments linking terrestrial 6G networks with satellite D2D overlays for critical infrastructure, automotive, and industrial IoT applications.

As demand for ubiquitous low-latency connectivity grows, terrestrial towers’ limitations—coverage gaps, high operational costs, infrastructure vulnerability—will induce stress on current capital allocation models favoring ground-based cellular expansions. Satellite D2D’s ability to deliver seamless continuity can attract investment and redraw industry boundaries, shifting spending toward space infrastructure and integrated hardware/software development.

This will force network operators and regulators toward structural adaptations including new spectrum allocation regimes for space-terrestrial hybrid services, harmonized protocols enabling interoperability across systems, and cross-sector governance frameworks addressing security and privacy in direct-to-device satellite communications.

Feedback loops may emerge as wider adoption reduces dependence on fiber and ground infrastructure, incentivizing private mega-constellation operators to expand coverage and innovate service delivery. Conversely, latency and capacity demands might prompt terrestrial networks to focus on hyper-localized ultra-dense deployments, intensifying competition but also heightening integration imperatives.

Under sufficiently broad regulatory harmonization and commercial viability, this evolution could dethrone the traditional hierarchical, cell tower-centric telecom model, ushering in distributed, resilient, and ubiquitous connectivity ecosystems with multi-stakeholder governance. This would recalibrate platform dominance, infrastructure ownership, and service provisioning models across sectors.

Why This Matters

From a capital allocation standpoint, incumbent telcos must evaluate new investment thresholds for integrating satellite D2D capability or risk disintermediation by space-native entrants who leverage vertical integration across hardware, software, and service layers. Industrial IoT players may need to architect devices capable of seamlessly switching between terrestrial and satellite device communication, redefining supply chains and vendor relationships.

Regulators face complex challenges to revise spectrum policies, certify security frameworks, and orchestrate cross-jurisdictional standards ensuring safe and fair competition between terrestrial and space operators. Liability frameworks governing data flows, service continuity, and failure scenarios may require recalibration, particularly affecting autonomous vehicle networks and critical infrastructure communication.

Strategically, governments and corporations positioned early could leverage integrated space-terrestrial D2D services for digital inclusion, defense communications resilience, and advanced mobility solutions, gaining competitive advantage in global innovation ecosystems.

Implications

The development may fundamentally transform telecommunications infrastructure investment from primarily terrestrial to hybrid space-ground platforms over the next two decades. It could reshape regulatory regimes, encouraging multilateral cooperation on spectrum, security, and operational governance.

This path is likely to support more resilient and geographically agnostic connectivity, accelerating IoT and autonomous mobility deployments. It is not a short-term incremental upgrade to 5G/6G but a disruptive re-architecture of connectivity fabrics.

This signal is not merely a hype cycle around Starlink or 6G commercialization in isolation. Rather, it represents a systemic potential inflection dissolving legacy infrastructure silos. However, competing interpretations might emphasize terrestrial 6G densification or emerging alternative low-earth orbit (LEO) constellations with limited interoperability as possible counterweights.

Early Indicators to Monitor

- Standardization progress on space-terrestrial D2D protocols, notably within ITU and 3GPP working groups.

- Capital flows toward satellite-integrated device chipset R&D and supplier partnerships linking satellite broadband with automotive and IoT manufacturers.

- Regulatory consultations proposing new spectrum allocation or cross-domain licensing models for hybrid services.

- Demonstrations or rollouts of pilot projects linking Starlink or equivalent constellations to terrestrial 6G infrastructure and mobile devices.

- Growth in patents around seamless handoff and device-managed routing between ground and space networks.

Disconfirming Signals

- Significant technological roadblocks in lowering device hardware costs or power consumption below commercial feasibility.

- Regulatory opposition to spectrum sharing or satellite/ground interoperability delaying policy framework development.

- Emergence of dominant terrestrial-only technologies that effectively address coverage and latency gaps.

- Market reluctance by industry actors to invest in dual-capable device ecosystems due to uncertain ROI or complexity.

Strategic Questions

- To what extent should capital investment pivot from terrestrial network expansions toward integrated space-ground infrastructures?

- How might regulatory frameworks evolve to balance competitive equity, security, and innovation in hybrid D2D connectivity?

Keywords

Device-to-Device Communication; Space-Based Internet; 6G Networks; Satellite Mega-Constellations; IoT Market; Regulatory Frameworks; Telecommunications Infrastructure; Autonomous Vehicles

Bibliography

- The United States Internet of Things Market was valued at USD 194.82 billion in 2025, is estimated to reach USD 244.89 billion in 2026, and is projected to reach USD 1,526.36 billion by 2034, growing at a CAGR of 25.7% from 2026 to 2034. Market Data Forecast. Published 10/04/2026.

- Low-latency, space-based Internet Starlink constellation could be integrated into Tesla vehicles, especially the Starlink Mini and future robotaxis and/or Optimus. Securities.io. Published 14/04/2026.

- 6G commercialization could begin by the end of this decade, marking a new era of hyper-connectivity. TechFueler. Published 15/03/2026.

- D2D opens the way for a fully converged space-terrestrial system around 2030, by the time sixth-generation (6G) mobile networks become the norm. ITU Hub. Published 09/04/2026.

- The global connected device population reached 21.1 billion at the end of 2025, growing 14% year-over-year and on a 13.2% CAGR trajectory toward 39 billion by 2030, per IoT Analytics' State of IoT 2025. Stingrai.io. Published 04/2026.

- 5G in 2026 will be shaped by standalone adoption, ecosystem readiness and the ability of operators to translate technical capability into commercial value. GSA Comm. Published 20/04/2026.