Unlocking Complexity: The Emerging Wildcard of Geo-Socioeconomic Fragmentation in Critical Resource Scarcity

Water scarcity and mineral supply constraints dominate discourse on resource scarcity, yet a subtle yet potent wildcard—accelerating geopolitical and socioeconomic fragmentation around critical resources—is emerging. This signal, grounded in growing bilateral trade alliances, export controls, and localized competition, could reshape capital flows, regulatory frameworks, and industrial ecosystems worldwide. Understanding this inflection is crucial for decision-makers anticipating how resource scarcity might catalyse systemic realignments beyond conventional environmental or technological narratives.

While climate-induced water scarcity and mineral shortages routinely headline risk analyses, a non-obvious development is the concurrent rise of strategic stockpiling and bilateral mineral trade agreements that fragment traditional supply chains. This geopolitical-economic fault line poses cascading effects on industrial sourcing, investment risk, governance structures, and regulatory regimes in the next 5–20 years.

Signal Identification

This development qualifies as a wildcard due to its disruptive potential combined with relative under-recognition in mainstream resource scarcity and industrial strategy discourse. Unlike well-identified climate-driven shortages or supply-demand imbalances, this is a socio-technical-political inflection—characterized by deliberate statecraft and international alliances—that could restructure global resource flows and control mechanisms.

The horizon for material impact spans from medium (5–10 years) as bilateral trade agreements and export controls intensify, to long-term (10–20 years) systemic fragmentation of global resource markets. The plausibility band is high given observed export restrictions and alliance formations.

Exposed sectors include critical mineral mining and refining, high tech manufacturing (semiconductors, batteries), water-intensive agriculture, heavy industry, and international trade governance.

What Is Changing

Traditional narratives focus on climate-driven resource scarcity—water shortages in southern Europe and India and agricultural stress under El Niño patterns (Blue Economy Observatory 15/06/2026; Elicit Plant 01/06/2026). Similarly, drought-driven water constraints in Turkey and UK regional vulnerability manifest growing environmental pressures (Hürriyet Daily News 18/05/2026; Kingfisher Press 01/11/2023).

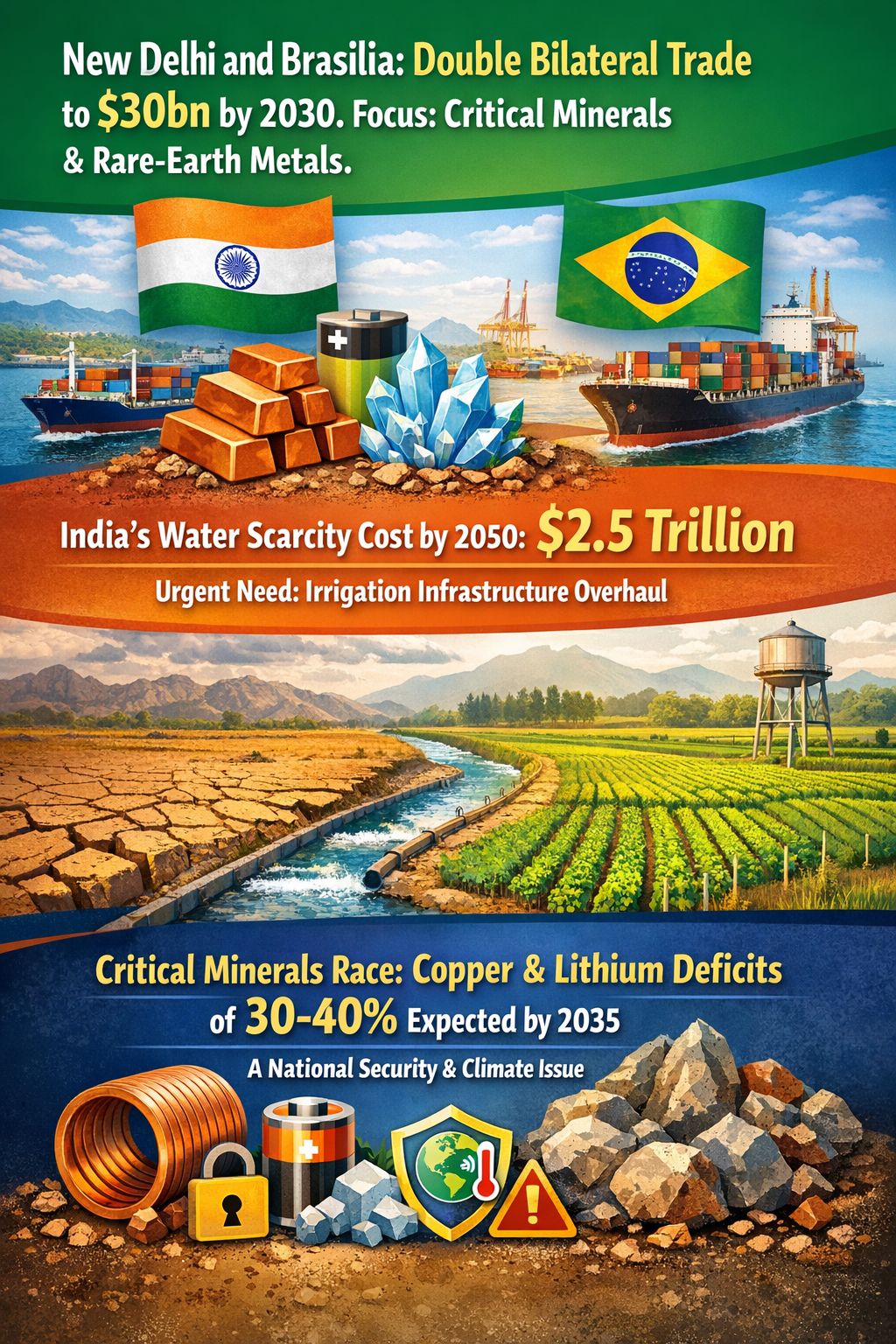

However, overlapping this environmental scarcity is a strategic geopolitical evolution: export controls on cobalt from the Democratic Republic of Congo and China’s rare-earth restrictions catalyse bilateral stockpiling and trade agreements—such as the doubling of critical minerals trade between India and Brazil—fragmenting global supply chains (Pomegra 13/05/2026; Al Jazeera 12/05/2026).

This trend transcends conventional supply-demand or climate-driven narratives by entrenching a new geopolitical economy layer. Rather than a single global market for scarce inputs, a patchwork of preferential resource blocs is emerging, incentivizing stockpiling and prioritizing politically aligned partnerships. Concurrently, the escalating competition over water-intensive resources and local water scarcity (e.g., SpaceX citing water limits on growth) indicates localized resource governance will increasingly shape industrial feasibility (iM Founder 15/06/2026).

This confluence creates an under-recognized systemic theme: fragmentation of resource governance and control, driven by geopolitical maneuvering layered atop environmental scarcity, producing discrete, localized resource blocs rather than globally integrated markets.

Disruption Pathway

Initially, export controls and political tensions amplify risks of supply disruption, prompting states and industries to accelerate bilateral agreements and stockpiles, prioritizing security of supply over cost efficiency. This drives capital allocation towards domestic mining capacity expansions and politically aligned partners, sidelining market liberalization and impeding multinational resource access.

As these arrangements deepen, the friction in global resource flows heightens. Fragmentation introduces inefficiencies but also hardens geopolitical boundaries around critical inputs, forcing multinational corporations to redesign supply chains for resiliency within politically favorable blocs.

This localized competition extends to water-intensive industries, where climate-driven water stress compounds operational risk, especially in water-scarce regions like southern Europe, Turkey, and parts of India (New Indian Express 25/05/2026). Regulatory frameworks will tighten regionally to protect scarce resources. Water scarcity thus becomes a gatekeeper not just environmentally but geopolitically and industrially.

Rising fragmentation triggers feedback loops as countries and firms hedge risks via strategic reserves, raising barriers to entry and promoting vertically integrated, territory-anchored industries. This dynamic undermines centralized governance models and global standards, necessitating new cooperative or competitive frameworks focused on resource bloc delimitation rather than universal market rules.

Consequently, dominant models of free-flowing global supply chains, multilateral governance, and open trade regimes could shift towards a segmented system defined by resource nationalism, alliance-driven trade, and regional regulatory regimes, affecting capital deployment, industrial location, and technology development trajectories.

Why This Matters

Decision-makers must recognize that resource scarcity risks extend beyond physical shortage to structural geopolitical and economic fragmentation. Capital allocation decisions favoring single-source suppliers or globalized supply chains may become riskier as supply security depends increasingly on political alignment.

Regulators may face pressures to incorporate geo-resource bloc dynamics into trade policy and environmental governance, adapting frameworks to multi-polar resource governance landscapes. Firms may have to recalibrate industrial strategies towards regional resource sufficiency and supply chain architecture resilient to bloc-based shocks.

Finally, this evolving landscape heightens operational, reputational, and compliance risks linked to sourcing from contested or politically sensitive regions, affecting investor risk assessments and liability frameworks in supply chain ethics and sustainability.

Implications

This wildcard could plausibly cause a fundamental realignment of resource economics from globally integrated markets to fragmented blocs, with potential to reshape capital flows, industrial ecosystems, and regulatory regimes.

The signal implies that supply chains might not merely adjust incrementally to scarcity but reconfigure in political-tectonic ways, prioritizing strategic sovereignty and alliance membership.

While it should not be conflated with simple protectionism or transient trade disputes, nor does it guarantee outright decoupling, this development likely indicates a durable shift toward multi-polar resource governance layered on environmental and technological scarcity.

Competing interpretations may see these trends as short-term crisis management; however, sustained export controls and alliance-building suggest deeper systemic reordering in the 5–20 year horizon.

Early Indicators to Monitor

- Expansion of bilateral and multilateral critical minerals trade agreements beyond existing frameworks

- Growth in state-led strategic stockpiling initiatives for water-intensive and mineral commodities

- Regulatory enactment of localized water usage restrictions affecting industrial sectors

- Corporate capital redeployment towards geographically aligned resource extraction and processing assets

- Formation of new international standards or governance bodies reflecting segmented resource blocs

Disconfirming Signals

- Reversal or easing of export controls on key minerals by dominant suppliers

- Emergence of comprehensive multilateral agreements restoring open resource trade and cooperative stockpiling

- Technological breakthroughs enabling substitution or dematerialization reducing demand for contested inputs

- Significant investments into global water infrastructure mitigating localized scarcity

- Consolidation of global regulatory standards overriding regional protectionism

Strategic Questions

- How should governments and firms adapt capital allocation strategies to navigate an increasingly fragmented resource governance environment?

- What regulatory innovations could balance localized resource sovereignty with the efficiencies and stability of global supply chains?

Keywords

Water scarcity; Critical minerals; Geopolitical fragmentation; Resource nationalism; Supply chain resilience; Bilateral trade agreements; Export controls; Stockpiling

Bibliography

- Supply Chain Ethics: As consumer activism grows, Samsung could be targeted by campaigns on issues like planned obsolescence, labour rights at suppliers, or rare-earth mining ethics. Risk Intelligence Service. Published 20/05/2026.

- SpaceX specifically cited droughts, water scarcity, local competition for resources, and regulatory restrictions as potential threats to future growth. iM Founder. Published 15/06/2026.

- Under climate change, many regions in the EU - especially southern European Member States - and globally are expected to face severe water scarcity. Blue Economy Observatory. Published 15/06/2026.

- Export controls on cobalt from the Democratic Republic of the Congo, combined with China’s restrictions on rare-earth materials, have prompted nations to accelerate bilateral stockpiling agreements - a trend that fragments supply chains even as it reduces individual exposure to single-source risk. Pomegra. Published 13/05/2026.

- Recently, New Delhi and Brasilia have been deepening their strategic alliance, agreeing in February to double existing bilateral trade to $30bn by 2030, especially of critical minerals and rare-earth metals. Al Jazeera. Published 12/05/2026.

- Water scarcity driven by climate change could cost India $2.5 trillion by 2050 if irrigation infrastructure is not overhauled. New Indian Express. Published 25/05/2026.

- Turkey, which is not classified among water-abundant nations, could move closer to the category of countries experiencing water stress in the coming decades due to population growth and the mounting impacts of climate change. Hürriyet Daily News. Published 18/05/2026.

- By comparison, the North West, the North East and Yorkshire & Humber will be less vulnerable to severe water stress. Kingfisher Press. Published 01/11/2023.