The Quiet Inflection: Blockchain’s Transformative Role Beyond Carbon Credits in Green Finance

Blockchain technology is often cited for its potential to reform carbon credit markets, but an under-recognized inflection lies in its broader capacity to fundamentally reshape green and sustainable finance through enhanced transparency, data integrity, and regulatory compliance frameworks. This structural shift could alter capital flows, regulatory regimes, and industrial configurations over the next decade, far beyond current expectations.

While carbon credit markets remain marginal in the broader climate finance ecosystem today, blockchain’s ability to underpin reliable, real-time data auditing combined with advanced analytics presents a genuinely non-obvious pivot point. Emerging regulatory demands and escalating sustainability expectations create conditions primed for this innovation to scale from pilot to systemic transformation.

Signal Identification

This development qualifies as an emerging inflection indicator. Although blockchain in carbon markets is recognized, the broader systemic roles it can play—such as enabling enforceable green finance due diligence, facilitating distributed real-time environmental, social, and governance (ESG) data verification, and automating regulatory compliance—is less appreciated. The horizon for this structural shift is within 5–10 years, driven by medium to high plausibility as regulatory standards tighten and capital markets demand verifiable sustainability data. Key sectors exposed include financial services, regulatory bodies, carbon markets, and climate risk analytics.

What Is Changing

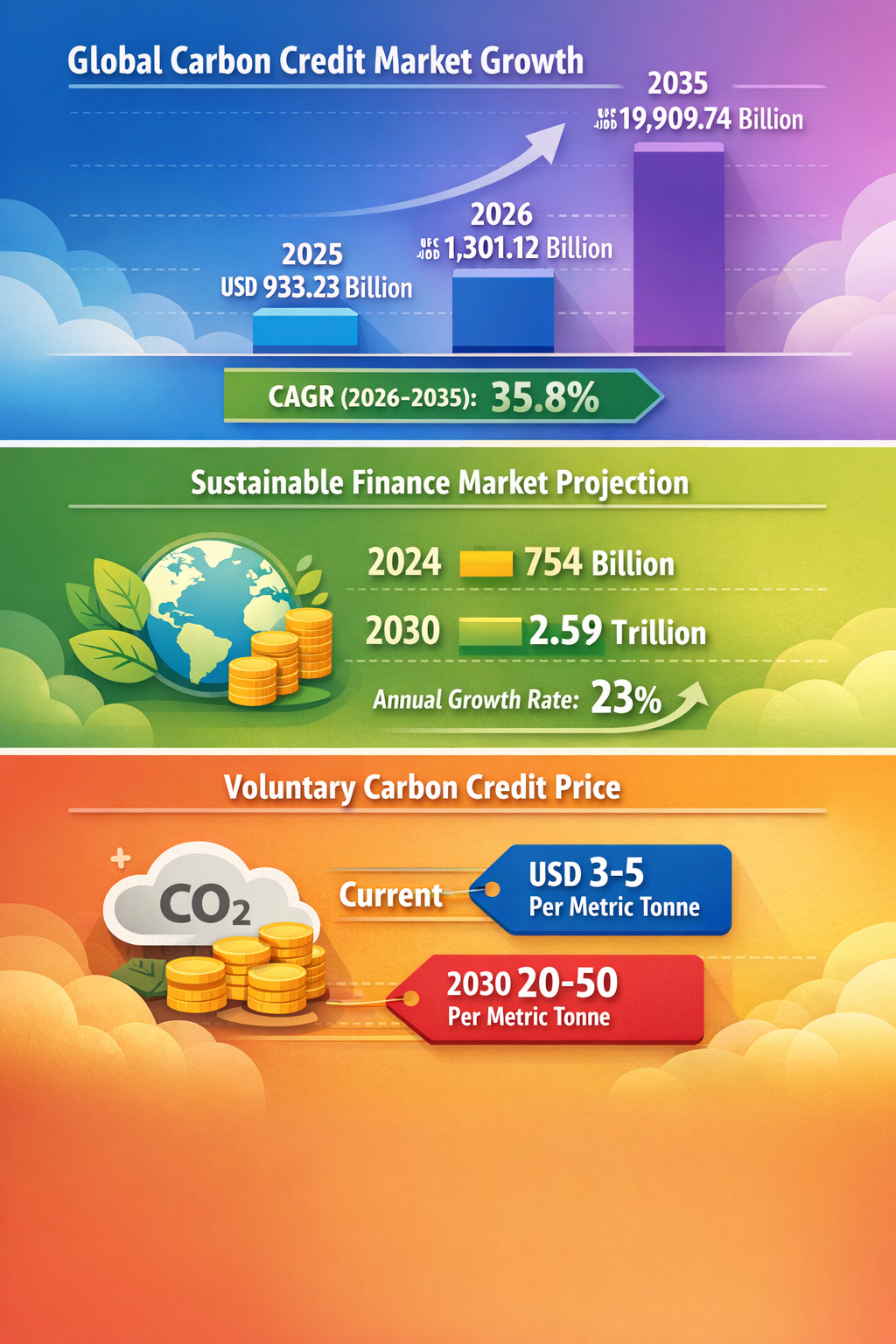

Three convergent developments from the assembled sources frame this shift. First, the carbon credit market is poised for massive growth, yet currently faces challenges of data credibility and transparency (Precedence Research 12/01/2024). Blockchain technology can uniquely address these issues through immutable ledgers, providing trust and traceability in transactions.

Second, regulatory bodies and investors are pushing for heightened data and disclosure standards for sustainable finance instruments (Hospitality Net 15/02/2024). This demand for real-time, reliable ESG data creates a fertile environment for blockchain-augmented analytics platforms that can automate reporting and reduce compliance costs.

Third, carbon markets remain relatively small compared to global green finance needs but offer a testing ground for private investment mobilization, dependent on credible, scalable data frameworks (Brookings 20/03/2024). Blockchain could act as the underlying infrastructure enabling this scale, ensuring credibility, reducing fraud, and facilitating international cooperation.

What is genuinely new is the recognition that blockchain’s value proposition transcends niche carbon credit applications, moving toward an integrated platform solution that could redefine capital allocation by assuring authenticity and enabling dynamic rebalancing of green assets and liabilities. This could disrupt existing audit, verification, and compliance intermediary roles.

Disruption Pathway

Blockchain-enabled green finance platforms may initially grow by integrating carbon credit registries with data analytics tools, improving transparency and liquidity. Accelerating factors include international regulatory mandates for ESG disclosure and private sector demands for verified sustainability claims.

As trust in these blockchain-based disclosures deepens, capital market participants may shift allocations toward green instruments with robust, enforceable data backstops. This shift would create stress on traditional verification and certification industries, forcing them to either adopt blockchain technology or become obsolete.

Regulatory bodies are likely to evolve, creating standards that mandate or strongly encourage blockchain-enabled reporting for climate-related financial disclosures. Such regulations will institutionalize these technologies, reinforcing feedback loops as firms innovate in data provisioning and risk management to capture green finance premiums.

Unintended consequences could arise from over-reliance on blockchain data integrity, potentially neglecting qualitative aspects of sustainability or creating new cybersecurity and privacy vulnerabilities. However, the net effect would elevate the systemic accountability of green finance, potentially shifting dominant governance models from fragmented voluntary disclosures toward more integrated, enforceable regimes with blockchain as backbone.

Why This Matters

For decision-makers, this signals a possible structural overhaul of sustainable finance frameworks. Capital allocation strategies may need to factor in blockchain-verified ecosystems that reduce greenwashing risks and increase confidence in sustainability claims. Regulatory frameworks might be redrawn to include technology standards, making compliance contingent on adopting blockchain-enabled transparency mechanisms.

Industrial actors within verification, auditing, and reporting sectors may face existential pressures, while technology firms could emerge as pivotal gatekeepers of green finance data infrastructure. Supply chains upstream might also come under increased scrutiny due to the enhanced traceability blockchain affords, compelling greater environmental and social compliance.

The governance implications span risk management, as regulators and investors gain tools for real-time climate risk assessment linked to verified data. Liability exposure may shift toward data inaccuracies or system vulnerabilities, raising new operational and legal challenges for financial institutions and corporate actors.

Implications

This development could likely catalyze a step-change in climate finance transparency and market integrity, enabling larger capital inflows into sustainable assets supported by verifiable data assurances. It may structurally alter the industrial landscape by marginalizing traditional auditing firms resistant to technological adoption, while elevating fintech players specialized in blockchain and data analytics.

However, this is not a panacea for all sustainable finance challenges. Blockchain’s role remains dependent on quality of input data, governance frameworks, and regulatory enforcement. Competing interpretations might argue that current ESG standard-setting bodies or centralized regulators could maintain primacy without wholesale blockchain integration.

The transformation is more evolutionary than revolutionary but driven by cumulative regulatory, investor, and technological pressures, making it a durable systemic change rather than transient hype.

Early Indicators to Monitor

- Emergence of regulatory draft standards referencing blockchain for ESG reporting and carbon market transparency

- Increases in venture funding specifically targeting blockchain-enabled environmental data analytics platforms

- Partnership announcements between traditional verification firms and blockchain fintech innovators

- Proliferation of blockchain-based carbon credit registries expanding linkage across jurisdictions

- Capital reallocation trends favoring green assets with technology-verified sustainability credentials

Disconfirming Signals

- Regulatory decisions rejecting blockchain-based data systems in favor of centralized or conventional reporting frameworks

- Persistent technological barriers or cybersecurity incidents undermining confidence in blockchain data integrity

- Failure of market acceptance by major institutional investors or financial intermediaries

- Stagnation or contraction of carbon credit markets, limiting ecosystem scale needed for impact

Strategic Questions

- How can regulators balance the imperative for transparency with technological risks inherent in blockchain-based ESG data systems?

- What investments and partnerships should capital allocators pursue now to position for a blockchain-enabled sustainable finance future?

Keywords

Blockchain; Carbon Credits; Sustainable Finance; Data Transparency; Regulatory Compliance; ESG Reporting; Climate Risk Analytics

Bibliography

- Blockchain and data analytics are the technologies that holds potential to augments the carbon credit market's growth globally while creating job opportunities as well in the domain of data analytics. Precedence Research. Published 12/01/2024.

- While carbon credit markets remain small compared to global needs for climate finance, they hold considerable potential for mobilizing private investment to achieve global climate and energy transition goals. Brookings. Published 20/03/2024.

- Sustainable finance trends for 2026 will be driven by increased regulatory demands, higher data standards, and the need to finance real-world transitions and climate adaptation. Hospitality Net. Published 15/02/2024.

- Task Force on Climate-related Financial Disclosures. FSB TCFD. Published 22/06/2023.

- Regulation (EU) 2020/852 on the establishment of a framework to facilitate sustainable investment ("Taxonomy Regulation"). EUR-Lex. Published 18/06/2020.